Can ChatGPT Plan My Retirement? An Honest Answer

Chatbots explain retirement well — computing one is a different job. Where AI helps, where it tends to slip, and what a real plan requires.

Here's a sentence you may not expect on a software company's blog: we think ChatGPT is genuinely useful for retirement planning. Just not for the part most people try to use it for.

TL;DR: Chatbots tend to be good at explaining retirement. Computing one — thousands of linked calculations, kept consistent across 30-plus years, under rules that change every year — is an engine's job. The strongest setup uses both: the engine for the math, AI for the plain language.

What chatbots do well

Ask what a RRIF is or how the OAS clawback works, and you'll usually get a clear, patient answer. For learning the landscape, conversational AI may be one of the best study tools ever built. The trouble starts when the question becomes "will my money last?"

Where they tend to slip — at least today

- Facts blur across tax years. Canadian rules move constantly — the OAS clawback threshold changes annually ($95,323 for 2026 income), GIS adjusts quarterly — and a mixed-year answer arrives with full confidence.

- Arithmetic at scale. One 2025 finance benchmark found leading models falling from roughly 95% accuracy on simple lookups to near zero on multi-step calculations — and a plan is 30-plus years of steps, each feeding the next. Code tools help, but then you're auditing one-off software yourself.

- Ask twice, get two plans. Different numbers on different days, with no year-by-year ledger anyone can check.

Privacy, too: with some popular chatbots, consumer conversations are used to train future models by default unless you opt out.

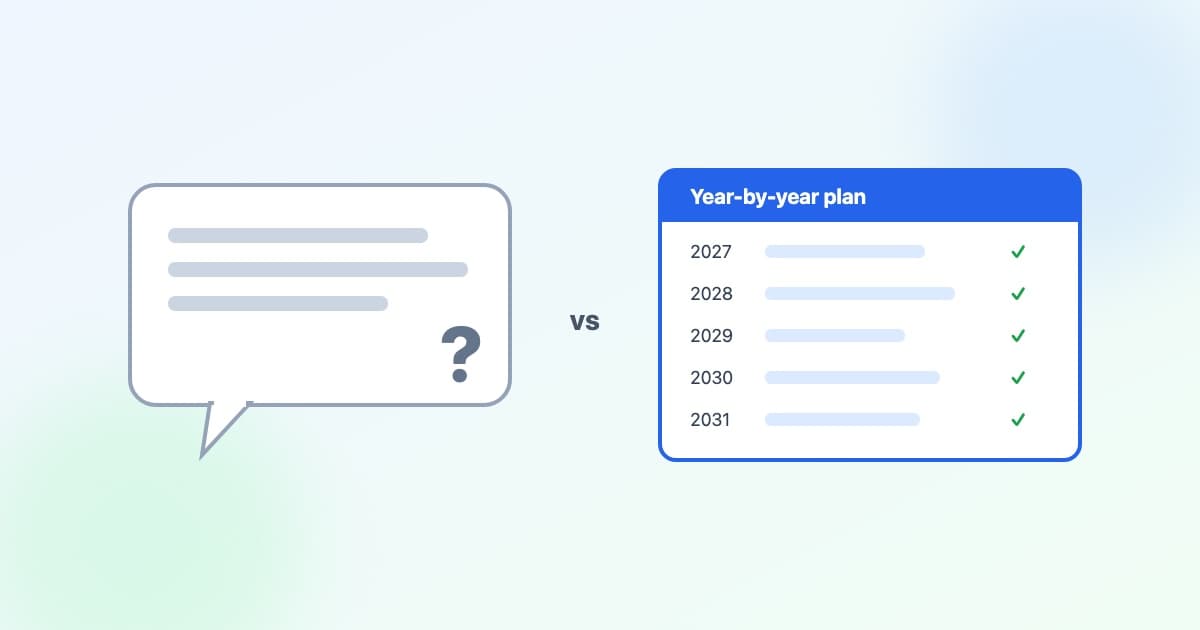

The right seat for AI

Retirement math interacts — withdrawal order changes taxes, which changes OAS clawback, which can change GIS, which changes the withdrawal. A dependable answer needs iteration until every year agrees, pinned current-year rules, and stress-testing that actually re-runs the plan — a simulation engine's basic job.

We're not anti-AI; parts of RetireZest are AI. The engine computes your plan deterministically under 2026 rules, and the AI explains what the numbers mean. Models will keep improving — this page describes mid-2026, not forever — and RetireZest will evolve right along with them, folding AI in wherever it genuinely helps you plan. Our bet: better AI gets better at driving engines, not replacing them.

Let the engine do the math

RetireZest computes your plan year by year under 2026 rules — and uses AI only to explain what the numbers mean.

Run my plan freeRetireZest is an educational retirement planning tool and does not provide personalized financial, tax, or legal advice. The calculations and projections are estimates based on current government rates and the information you provide. Always consult a licensed financial advisor or tax professional before making financial decisions. ChatGPT is a trademark of OpenAI; RetireZest is not affiliated with or endorsed by OpenAI.

Related Articles

Inflation Is Rising — Should Your Retirement Plan Change?

Canada's headline inflation jumped on gas prices. What monthly CPI numbers mean — and don't mean — for the inflation assumption in your retirement plan.

Canadian Retirement Numbers 2026: The Key Figures

CPP, OAS, GIS, TFSA, RRSP, RRIF minimums, and the 2026 tax thresholds that shape Canadian retirement plans — collected on one page.

Downsizing Your Home in Retirement: A Canadian Guide

What downsizing can free up, how the principal residence exemption works, and how to test a home sale in your retirement plan before you commit.