Canadian Retirement Numbers 2026: The Key Figures

CPP, OAS, GIS, TFSA, RRSP, RRIF minimums, and the 2026 tax thresholds that shape Canadian retirement plans — collected on one page.

Retirement planning in Canada runs on a handful of numbers that change every year — contribution limits, benefit maximums, clawback thresholds, withdrawal minimums. They're scattered across dozens of government pages, so we've collected the 2026 figures in one place. We refresh this page when new figures are released (most arrive each January; benefit amounts adjust quarterly).

TL;DR: For 2026 — TFSA limit $7,000; RRSP limit 18% of earned income up to $33,810; maximum CPP at 65 $1,507.65/month; OAS clawback begins at $95,323 of 2026 income; capital-gains inclusion stays at 50%; RRIF minimums start at 5.28% at 71.

CPP — Canada Pension Plan

| Figure (2026) | Amount |

|---|---|

| Maximum monthly pension starting at 65 | $1,507.65 |

| Start age range | 60 to 70 |

| Reduction for starting early | 0.6% per month (36% less at 60) |

| Increase for starting late | 0.7% per month (42% more at 70) |

| Year's Maximum Pensionable Earnings (YMPE) | $74,600 |

| Second earnings ceiling (YAMPE / CPP2) | $85,000 |

Few people receive the maximum — it takes close to 39 years of maximum contributions. Your own estimate is on your My Service Canada account. For how the start-age decision plays out, see when to take CPP. QPP figures for Quebec residents are closely aligned.

OAS — Old Age Security

| Figure (2026) | Amount |

|---|---|

| Maximum monthly payment, ages 65–74 | ~$752 (July–September quarter; indexed quarterly) |

| Maximum monthly payment, 75+ | ~$827 |

| Deferral increase | 0.6% per month (36% more at 70) |

| Clawback (recovery tax) begins | $95,323 of 2026 net income |

| Clawback for OAS paid July 2026 – June 2027 | based on 2025 income; begins at $93,454 |

| OAS fully clawed back (65–74) | $152,062 |

| OAS fully clawed back (75+) | $157,923 |

OAS amounts adjust every quarter with inflation, so the monthly figures above shift slightly during the year. The clawback removes 15 cents per dollar of net income above the threshold — our OAS clawback guide covers the common ways retirees manage it.

GIS — Guaranteed Income Supplement

| Figure (2026, indexed quarterly) | Amount |

|---|---|

| Maximum annual benefit, single | ~$13,300 |

| Income cutoff, single | ~$22,500 |

| Income cutoff, couple (both receiving OAS) | ~$29,700 |

| Clawback rate | 50 cents per dollar of income (single) |

GIS is income-tested but OAS itself doesn't count in the test, and neither do TFSA withdrawals — which is why account choice matters so much at lower incomes. Details in our GIS guide.

TFSA

| Figure (2026) | Amount |

|---|---|

| Annual contribution limit | $7,000 |

| Cumulative room since 2009 (never contributed) | $109,000 |

| Withdrawals count as income for tax / OAS / GIS? | No, under current rules |

Withdrawn amounts are re-added to your room on January 1 of the following year. Strategies in TFSA in retirement.

RRSP and RRIF

| Figure (2026) | Amount |

|---|---|

| RRSP contribution limit | 18% of prior-year earned income, up to $33,810 |

| Last year to contribute to your own RRSP | the year you turn 71 |

| RRSP must convert to RRIF (or annuity) by | end of the year you turn 71 |

RRIF minimum withdrawals (percentage of the account each year):

| Age | Minimum | Age | Minimum |

|---|---|---|---|

| 71 | 5.28% | 85 | 8.51% |

| 72 | 5.40% | 90 | 11.92% |

| 75 | 5.82% | 95+ | 20.00% |

| 80 | 6.82% |

A younger spouse's age can be used to lower the schedule. Full table and strategies in RRIF minimum withdrawal rates.

Tax figures worth knowing

| Figure (2026) | Amount |

|---|---|

| Lowest federal tax rate | 14% (reduced from 15% by Bill C-78) |

| Capital-gains inclusion rate | 50% — the proposed increase to 66.67% was cancelled |

| Pension income splitting | up to 50% of eligible pension income (RRIF income from age 65; Form T1032) |

| Federal pension income amount | $2,000 credit base |

| Principal residence sale | generally tax-free, but must be reported (Schedule 3 + T2091) |

Provincial rates vary — best province to retire compares them.

Seeing your own numbers

Limits and thresholds are the raw material; what matters is how they interact in your plan — which accounts you draw first, when each benefit starts, and where your income lands against the clawback lines year by year. RetireZest runs that simulation with the 2026 figures above built in, for Alberta, BC, Ontario, and Quebec, and your Zest Score summarizes how the pieces fit.

Figures from Canada.ca (Service Canada quarterly benefit tables, CRA registered-plan limits) as of July 2026. Quarterly-indexed amounts are marked approximate.

See how this applies to your plan

RetireZest models your exact situation — CPP, OAS, taxes, and withdrawal strategies — so you can see real numbers, not estimates.

Start Planning FreeRetireZest is an educational retirement planning tool and does not provide personalized financial, tax, or legal advice. The calculations and projections are estimates based on current government rates and the information you provide. Always consult a licensed financial advisor or tax professional before making financial decisions.

Related Articles

TFSA in Retirement — 2026 Limits + Strategies

TFSA contribution limits, withdrawal rules, and strategies for tax-free retirement income in Canada. 2026 rates included.

Downsizing Your Home in Retirement: A Canadian Guide

What downsizing can free up, how the principal residence exemption works, and how to test a home sale in your retirement plan before you commit.

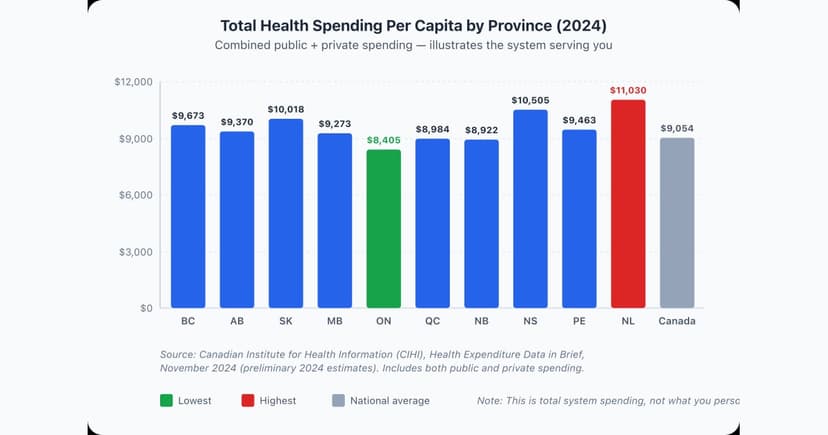

Healthcare Costs in Retirement Canada (2026 Budget Guide)

How much should Canadian retirees budget for healthcare? Out-of-pocket costs roughly $2,000–$6,000/year per person, plus drug coverage and long-term care fees by province.