Retirement Planning4 min read

Inflation Is Rising — Should Your Retirement Plan Change?

Canada's headline inflation jumped on gas prices. What monthly CPI numbers mean — and don't mean — for the inflation assumption in your retirement plan.

Expert advice on CPP, OAS, tax strategies, and withdrawal planning for Canadian retirees.

Canada's headline inflation jumped on gas prices. What monthly CPI numbers mean — and don't mean — for the inflation assumption in your retirement plan.

A 2026 fact-based look at Canadian retirement planning software — RetireZest, Optiml, ProjectionLab, MaxiFi, Canada.ca — by published price and features.

RetireZest is a free Canadian retirement planning tool that models CPP, OAS, GIS, RRSP, RRIF, TFSA, and corporate accounts under 2026 tax rules.

A practical 3-question test for whether you can retire in Canada — spending vs. income, where that income comes from, and why withdrawal strategy matters.

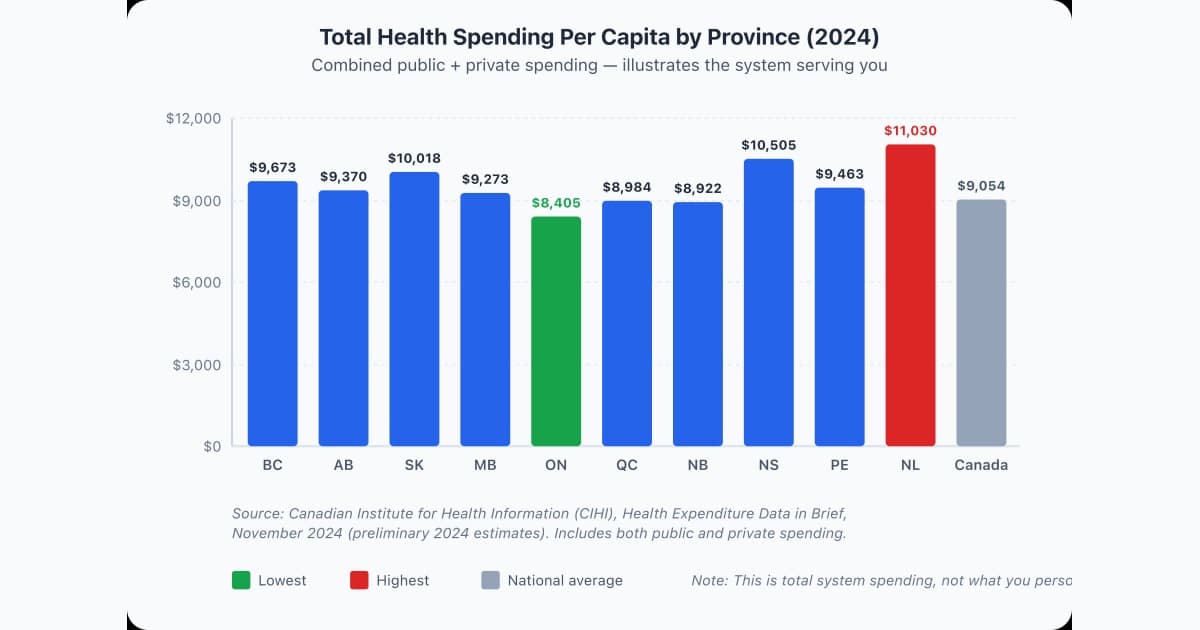

How much should Canadian retirees budget for healthcare? Out-of-pocket costs roughly $2,000–$6,000/year per person, plus drug coverage and long-term care fees by province.

Canadian retirees aged 65+ spend about $78,499/year ($6,540/month) on average — StatCan 2023. See the breakdown by category, couple vs single.

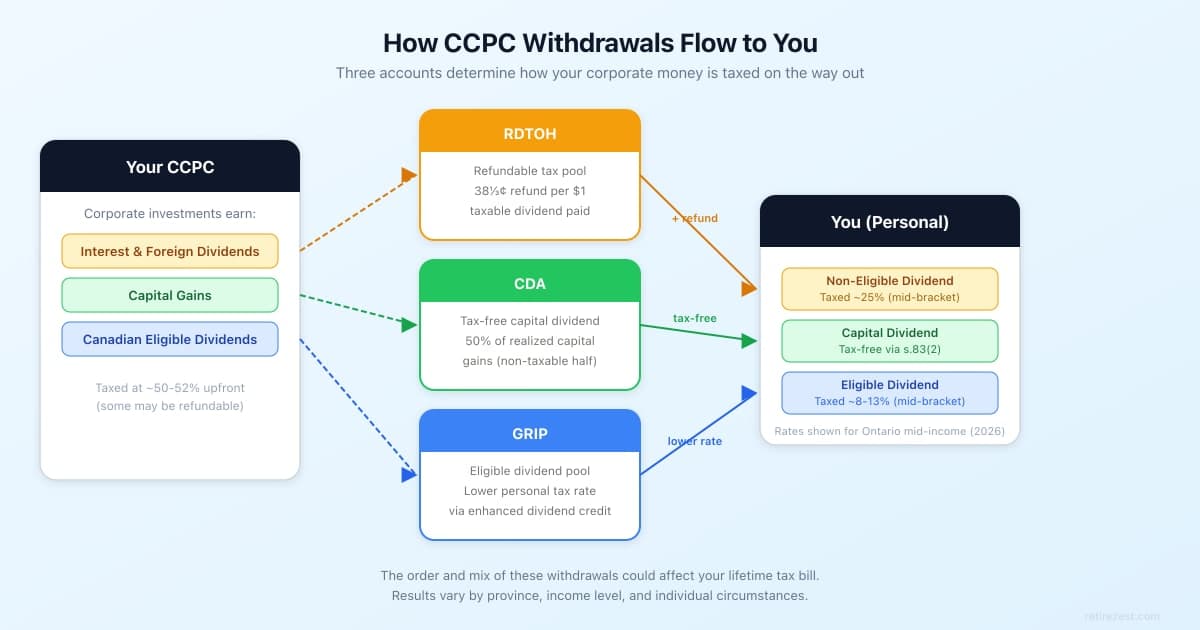

How CDA, RDTOH, and GRIP work for CCPC owners in retirement. The withdrawal method you choose may affect your lifetime tax bill.

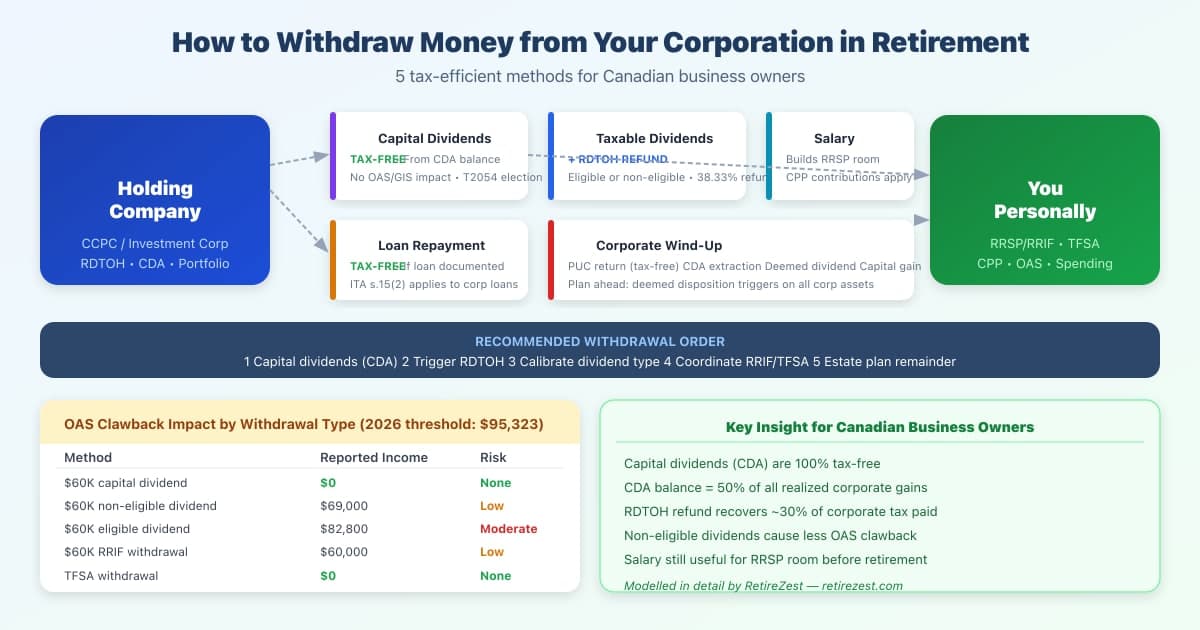

5 ways to extract money from your holding company in retirement — capital dividends, RDTOH, salary, dividends, and shareholder loans.

The Zest Score is a 0–100 retirement readiness score measuring plan survival, tax efficiency, cushion, and spending reliability.

RetireZest helps Canadians understand CPP, OAS, taxes, and withdrawal strategies through simulation. Educational tool, not financial advice.

Tax is one piece of where to retire. On tax alone: Ontario wins near $50K, BC near $80K, Alberta at $120K+. 2026 AB/BC/ON/QC comparison.

How to draw down your holding company in retirement. RDTOH, CDA, eligible vs non-eligible dividends, and withdrawal strategies.

When a CPP contributor dies, their spouse may receive a survivor pension. Learn how much, who qualifies, and how it affects your retirement plan.

GIS provides up to $1,109/month tax-free for low-income Canadian seniors. Eligibility rules, income thresholds, and strategies for 2026.

Your retirement "magic number" depends on lifestyle, province, and household size. Realistic 2026 targets with CPP/OAS factored in.

The GIS clawback reduces your benefit by 50 cents per dollar of income. 2026 thresholds and strategies to help protect your payments.

OAS clawback starts at $93,454 in 2026 ($95,323 on 2026 income). See the full thresholds, how the 15% recovery tax works, and 7 ways to avoid it.

Split up to 50% of eligible pension income with your spouse to reduce taxes. Rules, eligibility, and examples for 2026.

Canadian couples can reduce taxes by splitting retirement income. Pension splitting, CPP sharing, TFSA strategies, and coordinated withdrawals.

The CRA forces you to withdraw more each year — but the order you draw from RRIF, TFSA, and other accounts matters. 2026 rates by age + 5 strategies.

Draw down your RRSP early to avoid higher taxes later. How the meltdown strategy works, who benefits, and how to execute it.

Should you withdraw from your RRSP or TFSA first in retirement? It depends on your tax bracket, OAS clawback risk, and long-term plan.

Two retirees, same 30-year returns — one runs out of money, one doesn't. The difference is when the bad years hit. How to protect yourself.

TFSA contribution limits, withdrawal rules, and strategies for tax-free retirement income in Canada. 2026 rates included.

Taking CPP at 60 cuts your payment 36% (0.6%/month); waiting to 70 adds 42%. See the full age-by-age table, breakeven ages, and how to choose.