Can I Retire in Canada? A 3-Question Test (2026)

A practical 3-question test for whether you can retire in Canada — spending vs. income, where that income comes from, and why withdrawal strategy matters.

The short version. "Can I retire?" rarely has a "you need $X" answer. Three questions carry most of the weight: (1) does your income cover your spending year after year, (2) do you know where each income source comes from and when it starts, and (3) are you drawing in a tax-aware order? Get those right and you're likely in good shape — a full plan run can confirm it.

Three core questions

Plenty of questions matter in retirement — what to invest in, when to downsize, insurance, estate. Three of them carry most of the weight when deciding whether you can retire:

- Will income cover spending — every year, for the rest of your life?

- Do you know where that income comes from, and when each source starts?

- Are you withdrawing in an order that keeps the most money in your pocket after taxes?

Most online calculators answer only the first. That's why two people with identical savings can end up very differently: one retires comfortably for 30 years, the other runs out earlier or pays thousands more in tax than needed. In this article we'll walk through each question and show how RetireZest answers it — from tracking your real expenses to coordinating CPP, OAS, RRSP, and TFSA into a tax-aware withdrawal order.

Want the answer for your own situation? Try RetireZest — it runs the same three checks against your actual numbers in about five minutes. Free account required; no credit card.

What's RetireZest? A Canadian retirement-planning platform built for the rules retirees actually face — CPP, OAS, GIS, RRSP, RRIF, TFSA, and corporate (CCPC) accounts. It's a planning tool, not a bank or a financial advisor: you enter your numbers, the engine runs a year-by-year simulation under current CRA rules, and you see your retirement laid out from today through your 90s. Free to use; advanced features (PDF reports, Monte Carlo stress testing, the timing optimizer) are an optional paid upgrade.

Question 1: Your paycheque stops. Your bills don't.

Whatever your career looked like — employee, business owner, self-employed, or a mix — there's a date when the income you've been generating winds down. The mortgage, property taxes, groceries, healthcare, and the trip to Portugal don't.

The first question isn't "how much have I saved?" It's: can savings, government benefits, and any pension replace that income for the next 30 years?

Know your own number

The most useful first step is tracking your actual expenses for a few months — credit-card statements, bank withdrawals, autopay, cash. Many pre-retirees underestimate subscriptions, dining, gifts, and home maintenance. Once you have a realistic monthly number, the rest of the planning gets easier — you can plug it into any retirement plan, including the one in RetireZest.

Most retirees spend less — but not by half

Statistics Canada's Survey of Household Spending shows households aged 65+ spent roughly $60K/year on average — noticeably less than the ~$100K spent by households aged 55–64. Commuting, work clothes, and child-related costs tend to fall away. But the mortgage may persist into early retirement, and property taxes keep coming.

Plan for lumpy one-time expenses

A new roof, furnace, water heater, or vehicle is often a five-figure hit. So is helping with a child's wedding or a grandchild's education. A common rule: budget an extra $5K–$10K/year as a "lumpy expense" line, or hold a separate 3–6 month reserve outside the day-to-day plan.

Asset mix drives the plan as much as the dollar amount

Two retirees with the same savings can have very different outcomes depending on how the money is invested. Most plans assume a real (after-inflation) return of roughly 3–5% per year for a balanced portfolio — consistent with the FP Canada Projection Assumption Guidelines used by certified financial planners.

Whatever return you assume, stress-test against bad-sequence scenarios: a 30-year retirement will cross at least one significant downturn, and the order of returns matters as much as the average. See Sequence of Returns Risk.

Budget healthcare separately

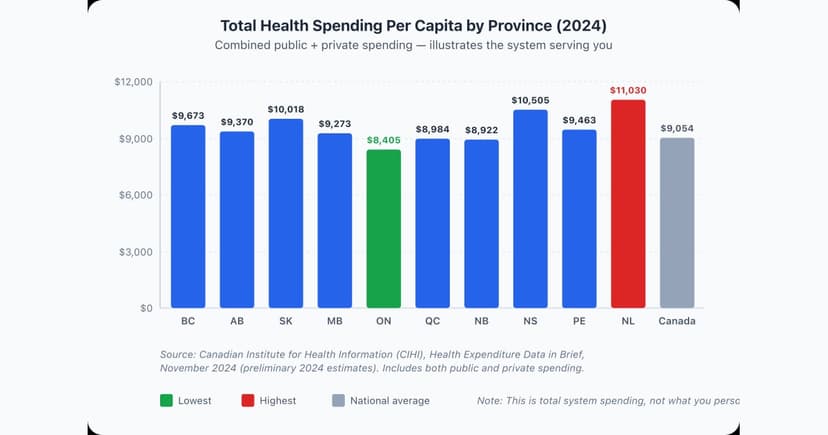

Provincial plans cover hospital and physician care, but prescriptions, dental, vision, hearing, physiotherapy, and any future long-term care are largely on you. See Healthcare Costs in Retirement Canada.

Plan past the average — that's your cushion

Statistics Canada life tables show that a Canadian who reaches retirement age can expect to live, on average, into their mid-80s (slightly later for women) — and that's the median. Half of retirees live longer than that, and a meaningful share live past 90 or 95. For couples, the chance that at least one spouse is alive at 90 is higher again. A common planning horizon is age 95 or beyond.

Anything left over isn't waste — it's the retirement cushion that absorbs longer-than-expected life, weaker markets, and surprise healthcare costs.

RetireZest produces a Zest Score for every plan — a 0-to-100 retirement-readiness score, similar in spirit to a credit score for your retirement. It measures four pillars: whether your plan survives, how much you'll pay in lifetime tax, how big your retirement cushion is, and how reliably your spending plan gets met. The cushion is the third pillar — for the same reason it's an anchor here in Question 1: it's what absorbs the things you can't predict.

The useful framing isn't "do I have enough?" It's "for how many years can my income cover my spending?"

How RetireZest answers Question 1. You enter spending in detail — three phases (active, moderate, quiet years), the mortgage, healthcare, and one-time events on the years they happen. The engine then runs your plan year by year to age 95+, tracking whether income covers spending and where the gaps fall.

Question 2: Income comes from several places — not all at once.

You don't have one paycheque in retirement. You have four to seven streams, each starting at a different age and taxed differently:

CPP (Canada Pension Plan)

Based on what you contributed during your working years in Canada — so the amount depends on your earnings history. You choose when to start, from age 60 to 70 (the later you start, the larger the payment). Quebec residents receive QPP instead, which works similarly. See When to Take CPP.

OAS (Old Age Security)

Paid to most Canadian residents aged 65 or older — eligibility is based on years lived in Canada, not on whether you worked. You generally need 10 years of Canadian residency to qualify and 40 years for the full amount. High-income retirees see part of their OAS clawed back. See OAS Clawback.

GIS (Guaranteed Income Supplement)

A monthly benefit for low-income seniors who receive OAS — reduced as your taxable income rises (effectively a clawback). See How to Avoid the GIS Clawback.

RRSP / RRIF

A Registered Retirement Savings Plan is a retirement savings plan you establish, register with the CRA, and contribute to (on your own behalf or your spouse's). Contributions reduce your taxable income today, investment growth inside the plan is tax-sheltered, and withdrawals in retirement are fully taxable. An RRSP must convert to a RRIF (or be annuitized) by the end of the year you turn 71, after which the government requires a minimum withdrawal each year. See RRIF Withdrawal Rates.

TFSA

A Tax-Free Savings Account is a registered savings account that functions like an investment account. Unlike an RRSP, contributions are not tax-deductible (you contribute after-tax dollars) — but investment growth and withdrawals are tax-free at any age. The federal government sets a new TFSA contribution room amount each year, and any unused room carries forward; withdrawn room is restored the following calendar year.

The rest

Non-registered investments, employer pensions, corporate/CCPC accounts, rental income, and home equity round out the picture. Each is taxed differently and starts on a different timeline. For business owners, see Corporate Retirement Planning.

How RetireZest answers Question 2. Every income stream is modelled separately, with its real start age and tax treatment, so you see when each source kicks in and how they fit together year by year.

Question 3: The order you withdraw from your accounts matters.

Two Canadians with identical savings can end up very differently based purely on the order they draw down. Three things drive it:

1. The tax treatment. RRSP withdrawals are fully taxed; TFSA withdrawals aren't. Withdrawal order changes your tax bracket, OAS clawback exposure, and (for low-income retirees) GIS.

2. The forced minimums. Once you turn 72, the government forces minimum RRIF withdrawals that you can't opt out of. Combined with CPP and OAS, this can push a household into OAS clawback territory. See RRIF Withdrawal Rates.

3. The bridge years. If you retire at 60 but delay CPP or OAS to 70, you need a decade of bridge income from savings first.

That's the case for the RRSP Meltdown Strategy: draw down RRSP early — at favourable brackets, before the forced minimums hit — and arrive at 72 with a smaller RRIF. RetireZest's CPP/OAS Timing Optimizer then tests every CPP+OAS start-age combination against your specific plan to find the one that keeps the most money in your pocket.

How RetireZest answers Question 3. RetireZest compares eight different withdrawal strategies — including the RRSP meltdown — against your specific household, and ranks them by what you care about (a balanced result, the largest after-tax estate, the lowest lifetime taxes, or the most spending throughout retirement). Combined with the CPP/OAS timing test above, you see the dollar difference between the default plan and the smarter one — year by year, in plain language.

Curious what your three answers look like? Try RetireZest with your own numbers — savings, income, province, age. The engine will walk through your specific situation, not a generic one. Free; no credit card.

How RetireZest helps a couple like this

Take a typical Ontario couple — savings around $900K, both retiring at 65 — and the planning gets practical fast. RetireZest shows them:

- Whether their plan survives through age 95 with the spending they want, year by year

- The dollar difference between a default plan and a tax-optimized one — same savings, smarter sequence

- How different CPP and OAS start ages compare — sometimes a difference of tens of thousands over 30 years

- What forced RRIF minimums at age 72 will do to their taxable income, while there's still time to plan around it

- The trade-offs between leaving the largest estate, paying the lowest lifetime taxes, and spending more each year

The dollar gaps are real but depend on the specifics — savings, spending, benefits, province, life expectancy. The point isn't a specific number; it's having those numbers for your household, before you retire.

Try RetireZest — free account, no credit card.

What affects your answer

Your answer depends on age at retirement (each year before 65 typically requires ~3% more savings), family situation (couples can split pension income, share TFSA strategies, and inherit CPP survivor benefits), markets (a 30-year retirement needs to survive the worst-case sequence, not the average), taxes and province (see Best Province to Retire in Canada), and life changes like divorce, inheritance, downsizing, or a healthcare event. A good plan bends; a fragile one breaks.

So — can you retire?

Answering these three questions with this knowledge helps you understand where you stand and brings you a step closer to clarity in your retirement.

Try RetireZest and walk through the three questions with your own numbers. It takes about five minutes — free, no credit card.

The goal isn't a perfect answer. It's reducing the uncertainty in your retirement plan.

See how this applies to your plan

RetireZest models your exact situation — CPP, OAS, taxes, and withdrawal strategies — so you can see real numbers, not estimates.

Start Planning FreeEducational content only. Not personalized financial advice. Tax and benefit figures change annually; dollar amounts in this article are illustrative and current-year specifics live in the linked deep-dive posts (which we keep updated). Authoritative sources: Canada Revenue Agency, Service Canada, Statistics Canada, and FP Canada. Verify your own CPP and OAS estimates with Service Canada; verify tax calculations with a qualified tax professional.

Related Articles

How Much to Retire in Canada (2026)

Your retirement "magic number" depends on lifestyle, province, and household size. Realistic 2026 targets with CPP/OAS factored in.

Healthcare Costs in Retirement Canada (2026 Budget Guide)

How much should Canadian retirees budget for healthcare? Out-of-pocket costs roughly $2,000–$6,000/year per person, plus drug coverage and long-term care fees by province.

What Retirement Actually Costs in Canada (2026)

Canadian retirees aged 65+ spend about $78,499/year ($6,540/month) on average — StatCan 2023. See the breakdown by category, couple vs single.